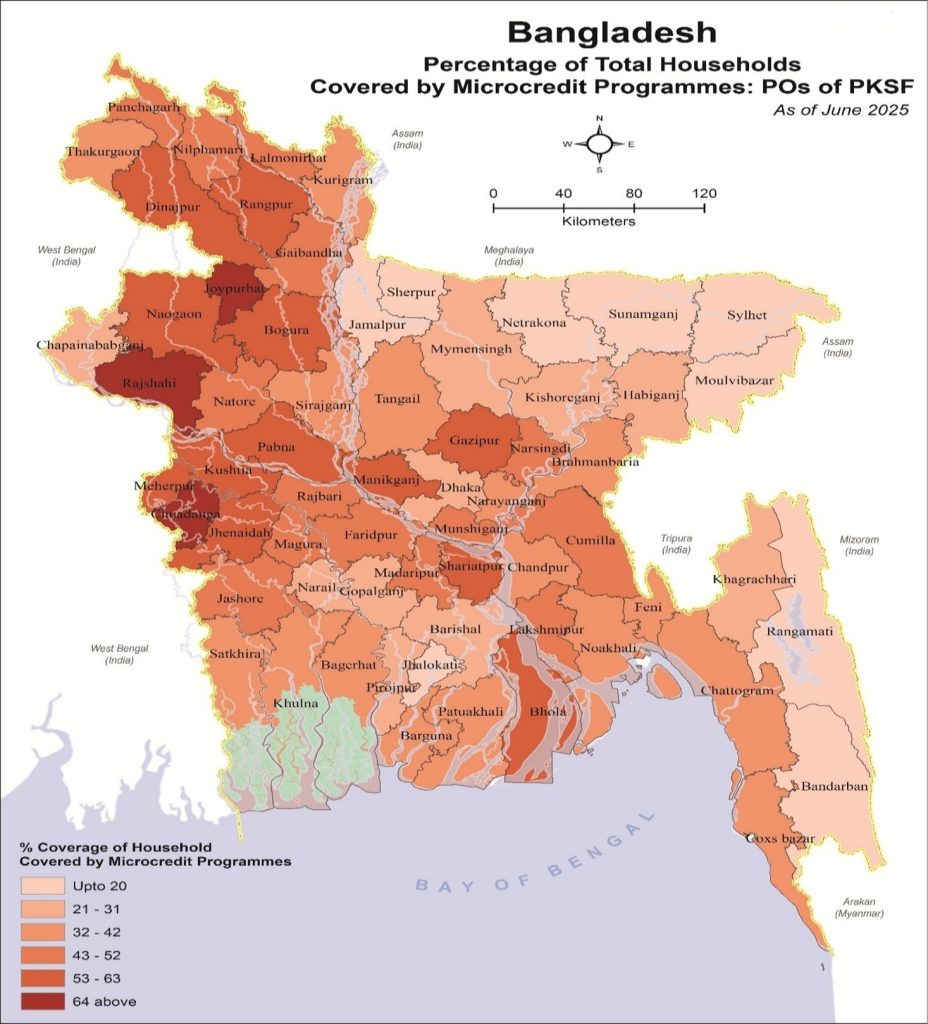

District-wise Loan Program Coverage:

With PKSF’s financial assistance, Partner Organizations (POs) are implementing loan programs across all 64 districts, 487 upazilas, and 12 city corporations of the country. An analysis of district-wise population and loan program data reveals that approximately 74% of total households in Chuadanga district are covered under the loan program the highest coverage among all districts. In contrast, only about 9% of total households in Sunamganj district are under the loan program the lowest coverage. Notably, in three districts, more than 70% of total households are covered under the loan program, while in 18 districts, less than 30% of total households are under coverage.

From Access to Empowerment: The Journey of Inclusive Finance

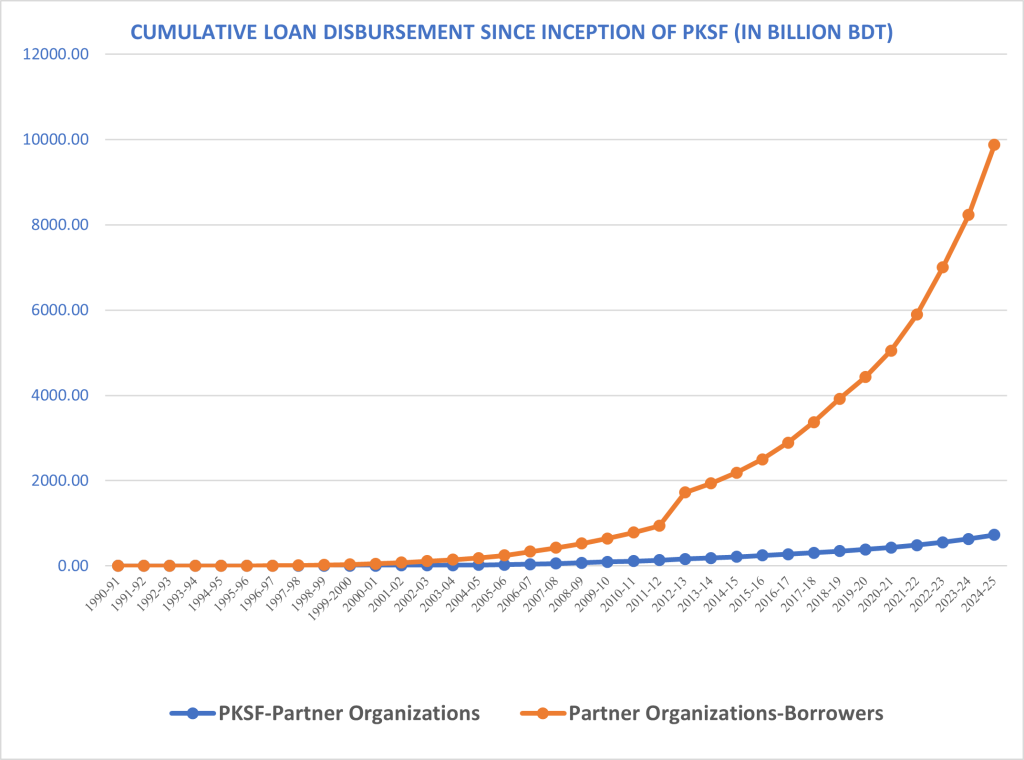

Cumulative Loan Disbursement

PKSF has evolved from a microcredit apex organization to a comprehensive livelihood-promoting institution. Its lending activities are structured to promote financial inclusion, entrepreneurship, and resilience across multiple sectors. Collectively, PKSF’s Partner Organizations (POs) have disbursed over BDT 9.15 trillion among grassroots members since inception, covering rural, urban, and specialized programs. This continuous growth highlights PKSF’s focus on evidence-based lending and development-oriented financial inclusion.

(BDT in Billion)

FY Range | PKSF-PO Level | Growth (%) | PO-Member Level | Growth (%) | Remarks |

1990-1995 | 0.63 | – | 1.40 | – | Early microfinance expansion |

1996-2000 | 8.25 | 1209.52% | 28.73 | 476.85% | Rapid growth with new POs |

2001-2005 | 22.03 | 167.03% | 165.73 | 232.81% | Introduction of SME lending |

2006-2010 | 93.99 | 326.65% | 551.57 | 257.15% | Enterprise & sectoral diversification |

2011-2015 | 216.26 | 130.09% | 1969.92 | 105.30% | Integration of agriculture & value chains |

2016-2020 | 385.83 | 78.41% | 4044.28 | 126.25% | Digital MIS integration |

2021-2025 | 727.34 | 88.51% | 9150.22 | 476.85% | Inclusive & technology-driven finance |

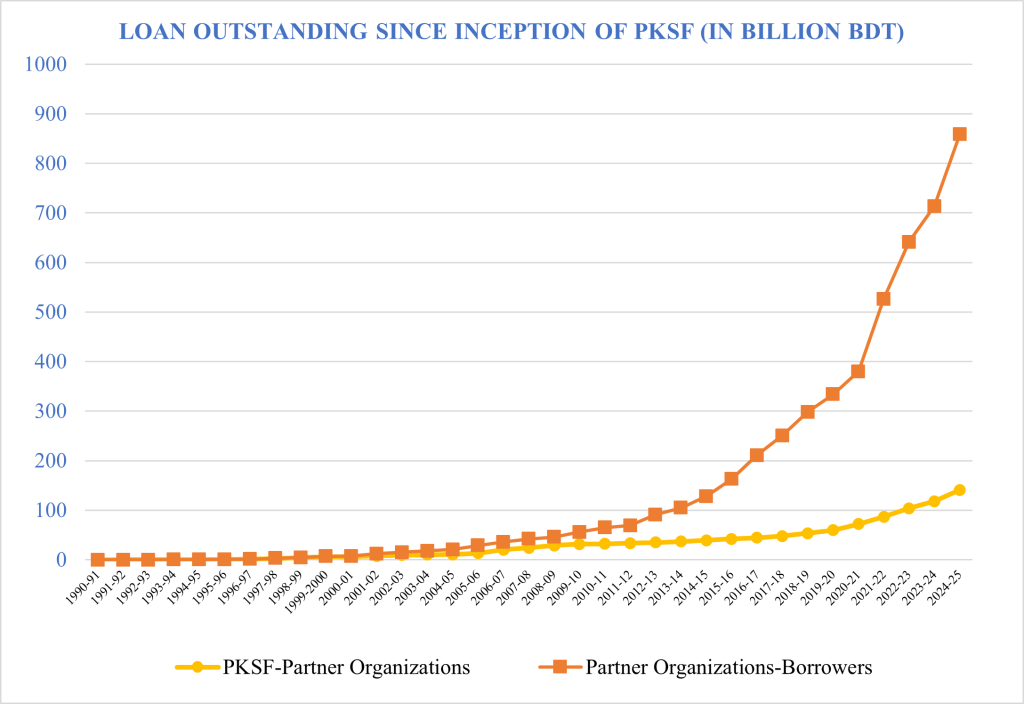

Loan Outstanding

The data shows a consistent and remarkable growth in loan outstanding amounts at both the PKSF-PO level and the PO–Member level over the past three decades. Starting from a baseline of 0.02 billion in FY 1990-91, both levels have shown exponential increases, reflecting PKSF’s expanding outreach and the increasing credit utilization capacity of Partner Organizations (POs) and also their members. By FY 1999-2000, the outstanding amount at the PKSF–PO level reached BDT 6.11 billion, while the PO–Member level stood at BDT 6.82 billion. This trend accelerated sharply thereafter, with the PO-Member level showing a faster growth rate by FY 2019-20, the figure was BDT 333.87 billion, compared to BDT 59.87 billion at the PKSF–PO level. FY 2024–25 indicates a significant escalation to BDT 141.05 billion and BDT 858.29 billion respectively, suggesting over six-fold growth within five years. This rapid increase underscores PKSF’s deepening financial engagement and the growing demand for microfinance at the member level.

(BDT in Billion)

FY | PKSF-PO Level | PO-Member Level | Remarks |

1990–91 | 0.02 | 0.02 | Baseline year operations initiated |

1994–95 | 0.46 | 0.48 | Early-stage disbursement activities |

1999–2000 | 6.11 | 6.82 | Expansion of PKSF’s credit programs |

2004–05 | 10.67 | 20.77 | Rapid increase in member-level outreach |

2009–10 | 31.63 | 55.99 | Consolidation and growth of lending portfolio |

2014–15 | 39.48 | 128.23 | Diversification of financial products |

2019–20 | 59.87 | 333.87 | Sharp rise in field-level credit flow |

2024–25 | 141.05 | 858.29 | Record expansion strong institutional capacity |

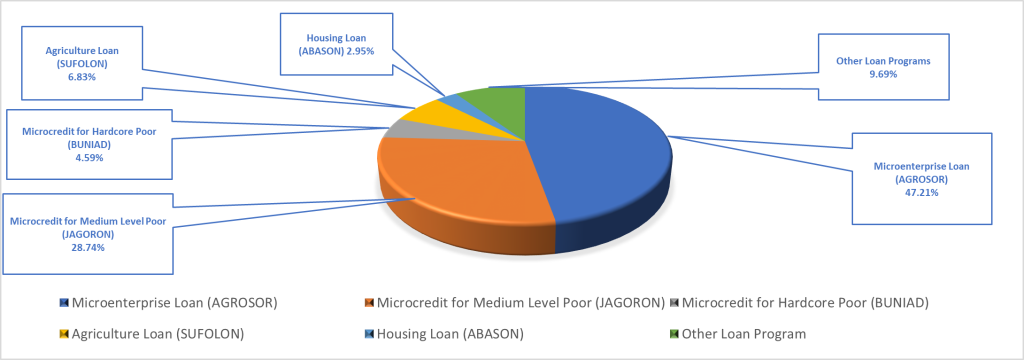

Sector-wise Loan Outstanding of PKSF at the Partner Organization (POs) Level

As of June 2025, the total loan outstanding of PKSF at the POs level stands at BDT 141.05 billion. Among this, BDT 66.59 billion belongs to the Microenterprise Loan (AGROSOR), BDT 40.53 billion to the Microcredit for Medium Level Poor (JAGORON), BDT 6.47 billion to the Microcredit for Hardcore Poor (BUNIAD), BDT 9.62 billion to the Agriculture Loan (SUFOLON), BDT 4.15 billion to the Housing Loan (ABASON) and BDT 13.67 crore to Other Loan Programs.

The percentage distribution of PKSF’s sector-wise loan outstanding at the POs level is as follows: Microenterprise Loan (AGROSOR) 47.21%, Microcredit for Medium Level Poor (JAGORON) 28.74%, Microcredit for Hardcore Poor (BUNIAD) 4.59%, Agriculture Loan (SUFOLON) 6.83%, Housing Loan (ABASON) 2.95%, and Other Loan Programs 9.69%.

% of PKSF’s loan outstanding by sector at the POs Level as of June 2025

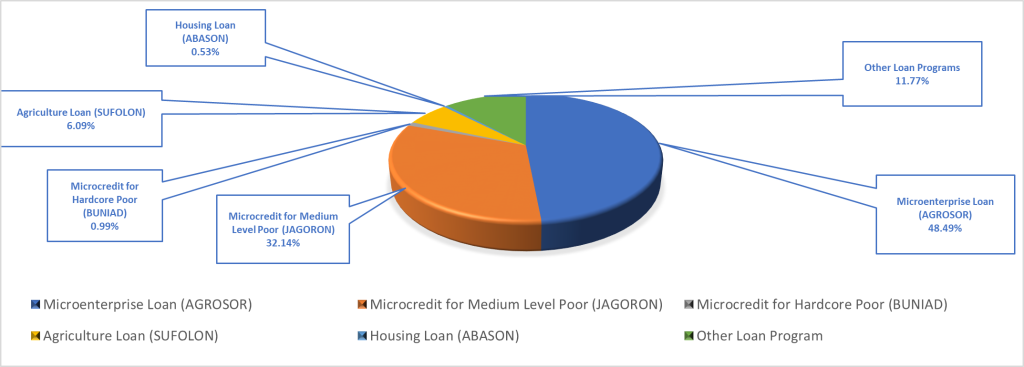

Sector-wise Loan Outstanding of Partner Organizations (POs) at the Member Level

As of June 2025, the total loan outstanding of POs at the member level stands at BDT 858.29 billion. Of this amount, BDT 416.14 billion belongs to the Microenterprise Loan (AGROSOR), BDT 275.83 billion to the Microcredit for Medium Level Poor (JAGORON), BDT 8.49 billion to the Microcredit for Hardcore Poor (BUNIAD), BDT 52.25 billion to the Agriculture Loan (SUFOLON), BDT 4.52 billion to the Housing Loan (ABASON) and BDT 101.03 billion to Other Loan Programs.

The percentage distribution of sector-wise loan outstanding of POs at the member level is as follows: Microenterprise Loan (AGROSOR) 48.49%, Microcredit for Medium Level Poor (JAGORON) 32.14%, Microcredit for Hardcore Poor (BUNIAD) 0.99%, Agriculture Loan (SUFOLON) 6.09%, Housing Loan (ABASON) 0.53% and Other Loan Programs 11.77%.

% of PO’s loan outstanding by sector at the Members Level as of June 2025

IN THE FINANCIAL

YEAR 2024-2025

WOMEN’S PARTICIPATION

0.70 MILLION NEW MEMBERS ENROLLED

OF THE TOTAL BORROWERS,

93.67% ARE FEMALE

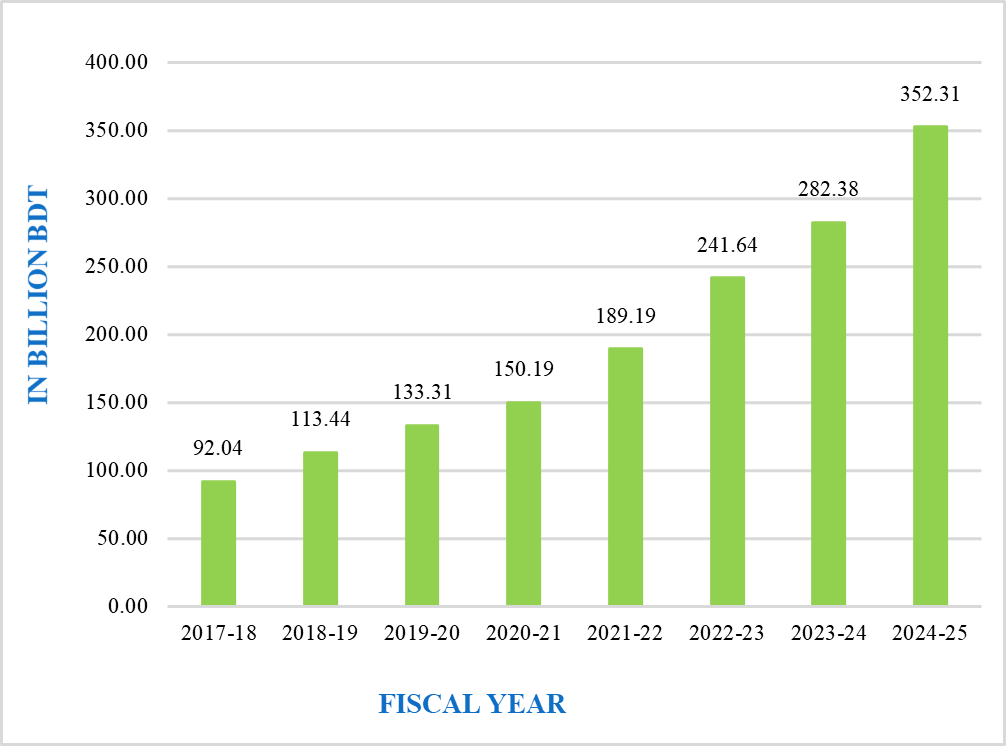

SAVINGS GROWTH OVER 8 YEARS

(IN BILLION BDT)